Real-time Payments

Countries all around the world are discovering and rolling-out real-time payment systems which enable people and businesses pay each other instantly. The most shining example of this is UPI the seminal flagship product of India’s premier payments institution, NPCI. UPI is expected to process 1 billion transactions per day by 2027. While players such as NPCI are changing the payments landscape in various countries, the rails laid-out by them are enabling other companies in creating point solutions which is leading to creation of new payment paradigms and even new businesses.

The world is now fully taken by the little squares wriggling inside a 3 cornered square. QR is Quite Remarkable.

Business milestones are about Customer Success, Traction, Revenues and EBITDA.

Funding helps you get there quicker and go farther.

You still get there yourself. And ‘earnings’ are not the same as number of followers and media mentions.

‘Solving for’, ‘Solved’ and ‘Solvent’.

Every startup is disrupting and innovating and ‘solving for’ something. Everyone has ideas. But the Customer wants what they find useful. Its not about what your product can do, it is about what people can do with it. Most startups fail because there is no need for the product. Companies are finding hard to create revenues, let alone earnings. At Alt-PI we have decades long track record of creating business which saw traction, usage and customer approval and more importantly, Revenues & EBITDA. No can do the canny ‘me-tricks’.

Regulations are Order, Rules-of-the-Game and Temperance.

Regulations are a fact of life for all players in the payments industry. They set the rules so that it is not a ‘fish market’. They also level the playing field and penalize the errants. Alt-PI believes adherence to regulations is not merely a ‘hygiene factor’ for business, it is a ‘health factor’. It makes the business sturdier and more robust. We believe compliance with the laws of the land is the original ‘regulatory arbitrage’, as it enables you to continue in business and often gain competitive advantage.

While startups keep innovating with their minds it is equally that they keep regulations in their head because institutionalized checks and balances are crucial for a stable ecosystem.

The Alternates:

Everything about collections.

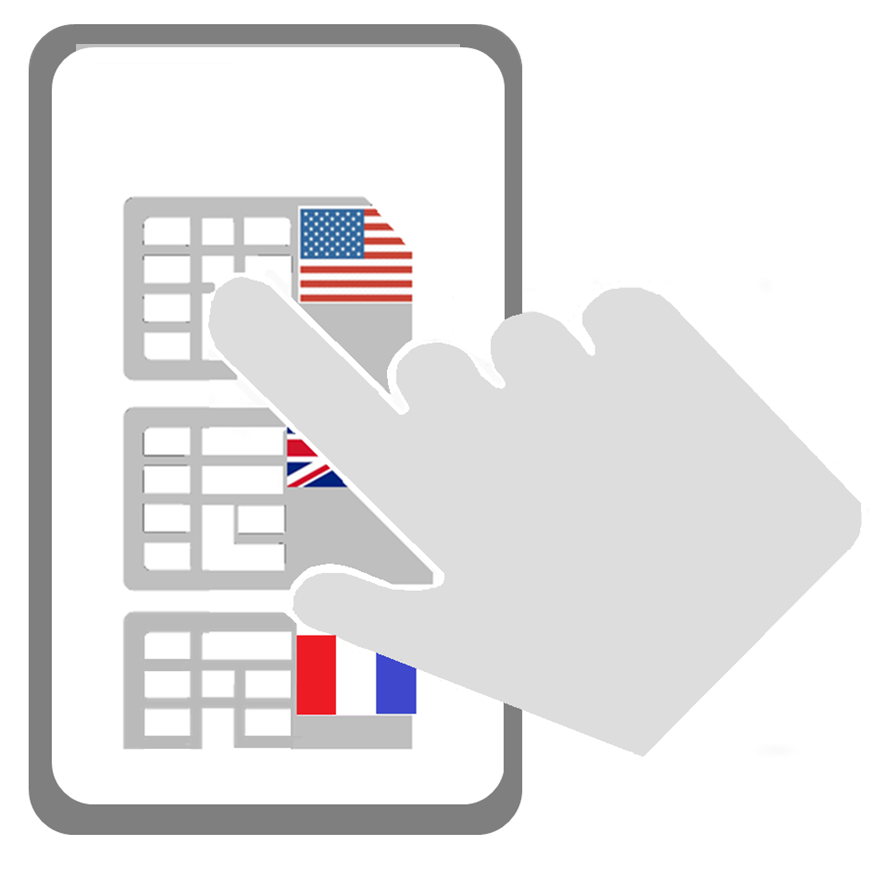

Kick-start Credit History where you study

Pay using the Local QR Codes.

Fish have fins. So ‘fintech’ is what, fishy?

Fintech is hard because the landscape is complicated, there are regulations and a history of growth through ‘purchased popularity’. Also, everyone is doing everything. There is no one who is not ‘disrupting’ and ‘innovating’. It seems to be more about the claque, the plaques and the clicks than business. At Alt-PI we build point solutions. We are too old to be knowing everything. We solve specific problems and provide measurable performance. We build platforms but also make sure that the ‘rails’ and the ‘rolling stock’ are in place so that the commerce happens. Platforms do become sleeping quarters pretty quickly.

Alt-Collect enables businesses to collect from their customers. Alt-Collect leverages real-time interbank payment systems and ‘mandates’ for future collections, where available.

This various types of collections include:

- Spot Collections. This includes payment links for pay-on-delivery, remote payer situations etc.

- Collection in Arrears. This includes bills payments for utilities, cards etc.

- Future Dated Collections & Mandates. This includes subscriptions, future bills, etc. These can be Collection Links generated on Due Date or Auto Debit Mandates.

| Utilities | Electricity, Gas – Piped Gas – Cylinders, Water | |

|---|---|---|

| Telecom | Post-Paid,Pre-Paid Recharge, Broadband, Datacard, Cable, DTH | |

| Transport | Pre-paid Tag Recharge, Metro Card Recharge, Railway Pass | |

| Financial Services | Loan Installments, Recurring Deposit Collections, Insurance Premia, Credit Card Bills, Mutual Fund SIPs | |

| Education | College Fees, Hostel Canteen Charges | |

| Board | Home Rentals, Hostel Rentals | |

| Memberships | Clubs, Diner Clubs | |

| Subscriptions | Print Media, OTT, Software Subscription Purchases | |

According to Thomas Cook, Indian students studying overseas spend $4 Billion every year. 65-70% of this money is spent in the USA. This figure is expected to go up to $ 8 Billion, over the next 4-5 years.

Currently, the student usually carries a card issued in India, or, puts in a deposit in an account gets a fraction of it as a ‘Card Limit’. In any case the Credit History for the student gets delayed by 2-3 years. So, a high-end low-risk customer in India becomes a low-end high-risk customer in USA as the Credit Bureaus don’t exchange notes.

Alt-Card solves for this. Alt-Card provides the student equitable and pragmatic ‘Card Limits’ in the country-of-study, backed by collateral assets in India (such as fixed deposits or real estate). The student gets a fair credit score immediately.

Current Options

| International Post-Paid Card |

|

|

|---|---|---|

| Secure Credit Card |

|

|

Alt-Card Option

- Best Exchange Rates

- Card Control

- Immediate Credit History

Add-on Products

- Automobile Loan

- Apartment Rent Deposit

- Insurance

- Hotel Options

QR Codes for everyone in SE Asia.

Travellers to leisure destinations in South East Asia are forced to keep cash for payments to small vendors as these vendors don’t accept cards (specially not, FX cards). They do accept local QR code based payments, but foreigners cannot pay using local QR. Or, Can they?

For the Europeans & British too?

So, how can it happen. QR codes are issued against local bank accounts and the foreigner does not have one. How does he/she pay using her bank account back home on Europe or UK or wherever?

With Alt-Pay? Yes.

Alt-Pay makes it happen. We enable the foreign tourist pay the local merchant using the local QR code (such as LankaPay or Duit) from his/her bank account. What is more we complay with GDPR and all security and data protection imperatives.

About

As many as 70 countries are putting in place, rails for real-time interbank payments and settlements. The entire payments ecosystem is undergoing a sea change. With NPCI’s UPI, India has been a leader and many products launched and tested in India are finding acceptance in other countries also.

Having been a part of the Indian ecosystem provides Indian payments professionals the opportunity to leverage their expertise in other countries.

Alt-PI is a company set by a team with extensive experience in the payments industry, now set to leverage it in other geographies and to go the extra mile in conceptualizing, where payments are headed, once these 70+ intra-country real-time payment systems are in place.

Executive Team Members

We are a group of technocrats who have known each other for a long time, and definitely not young enough anymore to know everything. Since disruption is the new normal, we have to be different just to fit in. Well. Here we are. With our experience. The hacks, the hiccups, the hits and the highs. Trying to conflate imagination and flights-of-fancy with existential bummers and reality checks.

Expert Team Members